For real estate investors, optimizing tax strategies is essential to maximizing the profitability of rental properties. One of the most powerful tools available is depreciation, a tax deduction that allows property owners to recover the cost of their investment over time. However, standard depreciation can be a slow process, prompting the question: Can you accelerate depreciation on rental property? The answer is yes, and a specialized approach called cost segregation can significantly enhance your tax savings. This article delves into the mechanics of accelerated depreciation, the critical role of cost segregation, and how investors can leverage this strategy to improve cash flow and investment returns.

What is Depreciation and How Does it Apply to Rental Property?

Depreciation is a tax mechanism that accounts for the wear and tear of a rental property over its useful life, as defined by the Internal Revenue Service (IRS). For residential rental properties, the IRS assigns a standard depreciation period of 27.5 years, while commercial properties are depreciated over 39 years. This means the cost basis of the property—excluding the value of the land—is divided evenly across these years, resulting in a consistent annual deduction.

For example, if a residential rental property has a depreciable basis of $275,000, the annual depreciation deduction would be approximately $10,000 ($275,000 ÷ 27.5 years). While this provides steady tax relief, the deductions are spread out over decades, limiting their immediate impact on cash flow. This is where accelerated depreciation offers a compelling alternative, allowing property owners to claim larger deductions in the early years of ownership.ay not be fast enough.

Understanding Accelerated Depreciation

Accelerated depreciation refers to tax strategies that enable property owners to deduct a greater portion of their property’s cost in the initial years, rather than spreading deductions evenly over the standard depreciation period. By front-loading these deductions, investors can significantly reduce their taxable income early on, improving cash flow and freeing up capital for reinvestment or property improvements.

The IRS allows certain components of a rental property to be depreciated over shorter periods—such as 5, 7, or 15 years—rather than the standard 27.5 or 39 years. These components include personal property (e.g., appliances or carpeting), land improvements (e.g., landscaping or parking lots), and specific building elements (e.g., specialized electrical systems or millwork). Identifying and reclassifying these assets is the key to accelerating depreciation on rental property, and this process is facilitated through a cost segregation study.

The Power of Cost Segregation

A cost segregation study is a detailed analysis performed by tax professionals or engineers to dissect a property’s components and assign them appropriate depreciation schedules. Instead of treating the entire property as a single asset subject to a long depreciation period, cost segregation breaks it down into categories eligible for faster depreciation. These categories typically include:

- Personal Property: Items like appliances, window treatments, carpeting, and furniture, which often qualify for 5- or 7-year depreciation schedules.

- Land Improvements: Exterior features such as fences, sidewalks, driveways, and landscaping, which may be depreciated over 15 years.

- Building Components: Certain structural elements, such as specialized plumbing, HVAC systems, or electrical installations, that can be separated from the main building structure.

By reclassifying these assets, a cost segregation study enables property owners to accelerate depreciation, claiming larger deductions in the first few years. For instance, a property with a $1 million depreciable basis might yield $100,000 in deductions over the first five years under standard depreciation. With cost segregation, the same property could generate $300,000 or more in deductions during that period by applying shorter depreciation schedules to eligible components.

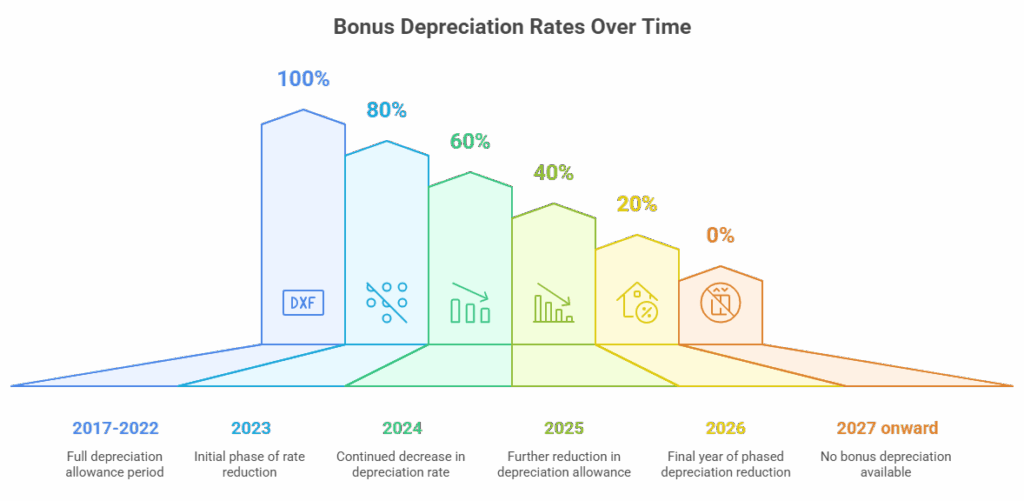

Bonus Depreciation: Supercharging the Benefits

As an added benefit, the IRS currently allows bonus depreciation on assets with a useful life of 20 years or less. That means qualified components identified in a cost segregation study can often be fully expensed in the first year.

Under the Tax Cuts and Jobs Act, 100% bonus depreciation was available from 2017 through 2022. However, it is now phasing out as follows:

- 2023: 80%

- 2024: 60%

- 2025: 40%

- 2026: 20%

- 2027: 0% (unless extended by legislation)

Even with the phase-out, combining cost segregation with bonus depreciation still offers substantial early-year tax savings.

Benefits of Cost Segregation for Rental Property Owners

Implementing a cost segregation study offers several advantages for investors seeking to optimize their tax strategy:

Strategic Flexibility: The increased deductions provide financial flexibility, allowing investors to weather economic downturns or fund property improvements.

Enhanced Cash Flow: Accelerated depreciation reduces taxable income, resulting in significant tax savings. This increased cash flow can be reinvested into additional properties, renovations, or other business ventures.

Tax Deferral: By front-loading deductions, investors can defer taxes to future years, potentially when they are in a lower tax bracket or have offsetting income.

Improved Return on Investment: The tax savings from cost segregation can boost the overall ROI of a rental property, making it a more lucrative investment.

Retroactive Savings: For properties owned for several years, a cost segregation study can be applied retroactively. Through a “catch-up” adjustment (via IRS Form 3115), investors can claim missed deductions from prior years without amending past tax returns.

Is Cost Segregation Right for You?

While cost segregation is a powerful tool, it may not be suitable for every investor or property. Consider the following factors:

Tax Situation: Investors with complex tax profiles, such as passive loss limitations, should consult a tax advisor to ensure cost segregation aligns with their overall strategy.

Property Value: Cost segregation is most cost-effective for properties with a depreciable basis of $500,000 or more. However, smaller properties can still benefit, especially if the investor owns multiple assets.

Holding Period: If you plan to sell the property within a few years, accelerated depreciation may lead to depreciation recapture, where the IRS taxes previously deducted amounts at a rate of up to 25%. Long-term holders typically benefit most.

Final Thoughts

If you’re serious about building wealth through real estate, don’t leave money on the table. Accelerated depreciation — especially when paired with a professional cost segregation study — can unlock thousands (even hundreds of thousands) in tax savings.

At CTA, we specialize in cost segregation studies that are both IRS-compliant and optimized to maximize your benefits. Contact us today to schedule a free consultation and see how much you could save.

We are also experts in green energy incentives and other programs related to real estate.