The passage of the One Big Beautiful Bill Act (OBBB) marks a major shift in the U.S. tax landscape—one that brings long-awaited relief for small businesses, real estate investors, and innovative companies. With sweeping updates to depreciation rules, R&D expensing, clean energy incentives, and more, 2025 presents a powerful opportunity to realign your tax strategy.

For taxpayers and their advisors, the new law offers both immediate deductions and long-term planning tools. But unlocking those benefits requires proactive action—especially before key windows close and incentives begin to phase out.

At Corporate Tax Advisors, we specialize in helping businesses capitalize on some of the most valuable provisions of the new law, including:

- Accelerated deductions through cost segregation studies

- Full utilization of R&D tax credits under the updated §174 rules

- Maximized benefits from Section 179D energy-efficient construction incentives

- Strategic access to Investment Tax Credits (ITC) and clean energy provisions

In this article, we break down how the OBBB affects each of these areas, what opportunities exist in 2025, and how businesses and CPAs can plan ahead to reduce tax liability, improve cash flow, and stay compliant.

Big Picture: OBBB’s Business Tax Provisions

The One Big Beautiful Bill Act (OBBB) introduces several transformative tax provisions aimed at stimulating domestic investment, innovation, and energy efficiency. While much of the media coverage focuses on individual tax relief and standard deduction changes, the most strategic planning opportunities for businesses lie in the expanded and restored incentives available beginning in 2025.

Here are a few key provisions that reshape the business tax planning landscape:

✅ 100% Bonus Depreciation — Permanently Restored

The OBBB reinstates and makes permanent the ability to immediately expense 100% of the cost of qualifying property in the year it’s placed in service. This revitalizes tax strategies around real estate improvements, equipment purchases, and building acquisitions—especially when paired with cost segregation to unlock short-lived asset classifications.

✅ Immediate Expensing of Domestic R&D Costs

The bill fixes a major pain point from recent years: under pre-OBBB law, domestic research expenses had to be amortized over 5 years. Beginning in tax year 2025, qualified domestic research expenditures can once again be fully deducted in the year incurred, restoring the powerful one-two punch of §174 and §41.

✅ Clean Energy Credits Begin to Phase Out

Although the Inflation Reduction Act (IRA) significantly expanded Investment Tax Credits (ITC) and production-based incentives, the OBBB introduces sunset provisions for many of these benefits. Solar, battery storage, EV charger, and other green energy credits will begin to phase down or expire between 2025 and 2026, prompting urgency for project sponsors and investors.

✅ Section 179D: Sunsetting Soon — Last Chance to Lock in Full Deductions

While the OBBB does not directly revise the mechanics of §179D, it codifies a permanent phaseout of the enhanced deduction values. As a result, projects that do not begin construction by June 30, 2026 will no longer be eligible for the current maximum $5.00 per square foot deduction. This creates a narrow window—primarily in 2025 and early 2026—for taxpayers to design and launch qualifying energy-efficient construction projects under the most generous terms available. Proper prevailing wage and apprenticeship compliance, documented in construction contracts from the outset, is now more essential than ever.

Why it matters:

These provisions are not just abstract changes—they unlock immediate cash flow, reduce quarterly estimated payments, and allow businesses to leverage the tax code as a financing tool for major investments. But each incentive comes with its own deadlines, documentation requirements, and coordination challenges—especially for taxpayers trying to combine multiple credits and deductions on the same project or tax year.

In the next sections, we’ll dive into how your business can leverage these incentives through targeted strategies in cost segregation, R&D, 179D energy deductions, and clean energy credits.

Cost Segregation: Leverage Full Bonus Before It’s Too Late

Among the most powerful provisions of the OBBB is the permanent reinstatement of 100% bonus depreciation. This creates a renewed window of opportunity for real estate owners, developers, and lessees to front-load deductions through strategic cost segregation.

What Changed Under the OBBB?

Previously, bonus depreciation was scheduled to phase down (80% in 2023, 60% in 2024, etc.). The OBBB reverses this decline and locks in 100% bonus depreciation for qualifying property placed in service starting in 2025, providing certainty and flexibility for long-term planning.

When paired with a cost segregation study, real estate owners can reclassify components of a building (e.g., flooring, HVAC, lighting, land improvements) into 5-, 7-, and 15-year property, making them eligible for immediate expensing.

Planning Tips for 2025

- Acquire or renovate property now with the intent to place it in service during or before 2025.

- If you acquired property in a prior year but haven’t done cost segregation, you may still qualify for a lookback 3115 adjustment to capture missed depreciation.

- For partial asset dispositions or tenant improvements, perform an updated cost seg to avoid leaving deductions on the table.

Who Benefits Most?

- Commercial real estate owners

- Multifamily developers and operators

- Triple-net lease investors and passive landlords

- Businesses that lease and improve their own space

Action Items

- Schedule a cost segregation feasibility review on any property over $500,000

- Coordinate timing of placed-in-service dates to maximize 2025 expensing

- Ask your CPA about Form 3115 to capture missed depreciation for prior years

Bottom line:.

With 100% bonus depreciation restored, cost segregation is once again one of the most impactful tools in the tax planning toolbox. But maximizing its value requires early coordination—especially if you also plan to claim other credits like §179D or the ITC on the same building

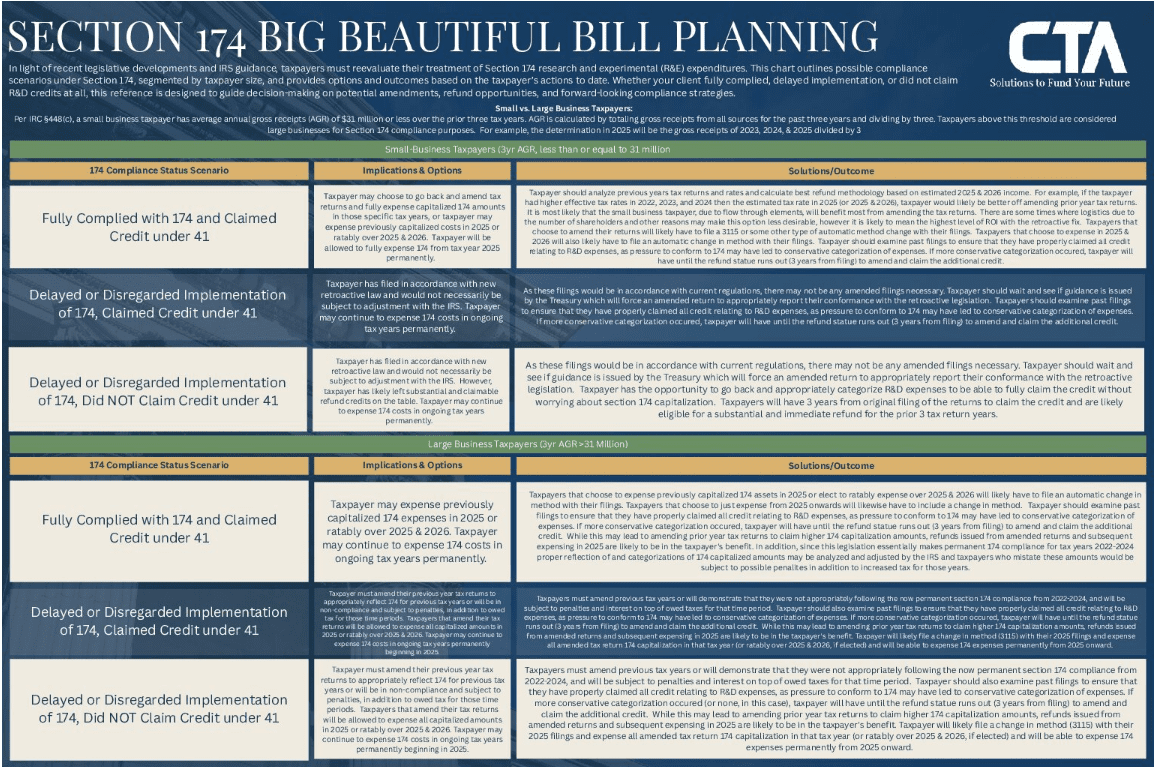

R&D Tax Planning in 2025: Refunds, Retroactive Relief, and the §174 Reset

Few tax provisions have created more frustration in recent years than the forced capitalization of domestic research expenses under §174. Introduced in 2017 and enforced starting in 2022, the provision required businesses to amortize R&D costs over five years—even when they otherwise qualified for the R&D tax credit under §41.

The One Big Beautiful Bill Act (OBBB) finally corrects course—restoring immediate expensing of domestic research beginning in 2025—and, for small businesses, opening the door to amended returns and tax refunds for prior years.

The §174 Fix: Immediate Expensing + Refund Rights for Small Businesses

Effective January 1, 2025:

- Domestic research and experimental (R&E) expenses are once again fully deductible in the year incurred.

- Foreign R&D remains subject to 15-year amortization.

- Small business taxpayers (average gross receipts ≤ $31 million over the past 3 years) are allowed to:

- Amend 2022–2024 returns to retroactively expense §174 costs and claim refunds, or

- Deduct remaining capitalized §174 amounts fully in 2025, or

- Elect to amortize over 2025 and 2026 if it creates a better tax outcome.

Refund Opportunity: What This Means for Small Businesses

If your company capitalized §174 expenses in 2022 or 2023 and you meet the small taxpayer test:

- You may be eligible to reclaim tens or hundreds of thousands in overpaid income taxes.

- IRS guidance will allow for streamlined Form 3115 filings or amended return processes.

- This applies whether or not you claimed the §41 R&D credit—any domestic R&D expense that was capitalized may now be fully deductible.

Planning Note: NOL Limitation Creates New Tradeoffs

For taxpayers who are not eligible to amend, but who must take amortization in 2025:

- The 80% net operating loss (NOL) limitation has been extended through 2026 under the OBBB.

- This means that large §174 deductions in 2025 may not immediately reduce taxable income, and excess deductions may be deferred.

- Taxpayers may wish to elect to amortize §174 costs over 2025 and 2026—especially if they can:

- Harvest capital gains in 2026 to absorb remaining deductions, or

- Match deduction timing to income forecasts to maximize current tax savings.

Takeaway: Taxpayers need to model both scenarios—immediate expensing vs. 2-year amortization—under the new NOL rules.

How Our Firm Helps

At Corporate Tax Advisors, we can:

- Identify all qualified R&D activities under §174 and §41;

- Prepare refund-ready amended returns for 2022 and 2023;

- Coordinate with your CPA to file Form 3115 or elect amortization under new 2025 rules;

- Maximize your §41 credit while safely integrating it with §174 deductions;

📌Action Plan for 2025

| Step | Why It Matters |

| Determine small business status | Only those ≤ $31M average receipts can amend prior-year returns |

| Identify capitalized §174 costs | Recover cash by expensing those costs now |

| Evaluate refund vs. amortization path | Balance NOL limits, income forecasts, and carryover benefits |

| Prepare updated §41 R&D credit study | Pair immediate deductions with valuable tax credits |

| Maintain strong documentation | IRS scrutiny will increase with refund claims and method changes |

Bottom line:

OBBB gives innovative businesses a rare opportunity to correct §174 compliance issues and unlock immediate cash benefits. For small businesses, it’s about getting paid back for what you already built. For others, it’s about strategically timing deductions in a way that beats the 80% NOL ceiling and delivers real tax relief—not just carryforwards.

Depending on your previous compliance with section 174, Corporate Tax Advisors has created a special one sheeter to compare and contrast your options. Download HERE.

.Section 179D: Last Call for the $5/sq ft Deduction — Construction Start Deadline Clarified

The One Big Beautiful Bill Act (OBBB) has cemented a critical deadline: projects must begin construction by June 30, 2026 to qualify for any Section 179D deduction, including the maximum $5.00/sq ft level available for 2025 projects that meet prevailing wage and apprenticeship requirements.

This “begin‐construction” cutoff is the core triggering event of the legislation—not placement in service. It determines eligibility permanently, and construction that starts on or after July 1, 2026, generally disqualifies the project from claiming the deduction at all.

What This Means Under OBBB

- The enhanced 179D deduction (ranging approximately from $2.90 to $5.81 per sq ft for 2025, depending on energy savings and compliance levels) is only available if construction commences by June 30, 2026

- After that date, the deduction phases out and is then permanently eliminated—this is not a temporary window.

- Projects starting after June 30, 2026 typically receive only a base deduction (around $0.58–1.16 per sq ft at most), and some may be entirely disqualified under current law.

Thus, 2025 project starts are critical—they lock in eligibility and maximize the economic value well into the phase-out period.

Contract Language: Build in Compliance From Day One

- To ensure eligibility for the full $5.00/sq ft deduction, contracts must require prevailing wage and registered apprenticeship compliance from the outset.

- Key provisions should include:

- Obligations for the general contractor to submit certified payroll reports.

- Requirements to use DOL-registered apprenticeship program labor.

- Audit-ready documentation covering hours worked, wage rates, and training milestones.

- Design professionals should insist on these clauses during the bid or contract negotiation stage, especially when expecting deduction allocation from a public or nonprofit owner.

Who Must Act Now

- Architects and engineers designing public sector, educational, healthcare, or nonprofit facilities—

- Building owners and developers planning new construction or retrofits that could qualify under 179D,

- Those coordinating 179D with cost segregation or ITC, particularly where the same property may generate multiple incentives.

Action Items for 2025

- Lock in a documented start of construction before June 30, 2026:

- Ideally within 2025, including pre-construction contracts or tangible expenditures to meet the 5% safe harbor threshold.

- Include explicit wage and apprenticeship clauses in all construction-related contracts.

- Initiate a §179D feasibility analysis aligned with energy modeling (ASHRAE standards) and allocation strategy.

- For public/nonprofit projects, secure allocation letters early (RFP stage if possible).

Why It Matters

There is no retroactive extension expected. Under OBBB, the rule is final: if construction begins on or after July 1, 2026, the enhanced deduction is gone—and often the entire benefit is lost.

With modeling, labor compliance, and contract negotiation often requiring months of lead time, any delay into 2026 could mean forfeiting hundreds of thousands—or even millions—in potential deductions. For 2025 planners and clients alike, this is truly the final window.

Investment Tax Credits: Clean Energy Benefits Begin to Sunset — Act Fast

Under the One Big Beautiful Bill Act (OBBB), clean energy tax credits—particularly the Investment Tax Credit (ITC) and Production Tax Credit (PTC)—are now subject to hard construction-start deadlines and major phaseouts, with the most expansive incentives vanishing entirely after mid‑2026.

For solar, wind, and other renewable energy projects, 2025 and early 2026 represent the final window to secure the full suite of tax benefits before they erode or vanish.

What’s New Under the OBBB?

- Wind and solar projects must begin construction by July 4, 2026 to remain eligible for tax credits under Sections 48E (ITC) and 45Y (PTC)

- Projects that start construction after July 4, 2026 must be placed in service by December 31, 2027 to claim any credits—otherwise, they lose eligibility entirely.

- Projects beginning construction before that date can generally rely on a four‑year placed‑in‑service window, meaning those beginning in 2026 may still qualify through 2030.

- These rules apply to commercial and residential solar, wind, energy storage systems, and EV charging projects seeking federal ITC / PTC credits.

Construction Start Deadline Is Non-Negotiable

The beginning-of-construction (BOC) trigger now overrides prior flexibility:

- You must pay or incur 5% of project costs by July 4, 2026 or begin significant physical work to satisfy the IRS BOC test.

- Contracts, site preparation, module procurement, and early civil work all count toward this threshold, but must be well-documented to withstand scrutiny.

- Treasury is expected to issue new guidance in mid‑August 2025 restricting abusive use of safe harbors—making early, substantive work more critical than ever.

Contract Language: Lock in Compliance Early

To preserve the enhanced ITC or PTC benefits and stack bonus credits, project contracts should include:

- Prevailing wage and registered apprenticeship compliance clauses, where relevant;

- Document retention obligations, including certified payroll, apprenticeship logs, and supplier verification for domestic content;

- Obligations tied to energy community or domestic content bonuses;

- Assignment of project-level responsibility for maintaining continuity toward placed-in-service.

Failing to incorporate these terms can reduce available credit by up to 80% or disqualify bonus components altogether.

Who Needs to Act Now?

- Commercial developers, project sponsors, and site owners planning solar, wind, battery storage, or EV charging installations.

- Municipalities, nonprofits, schools, and healthcare facilities pursuing new clean energy builds via Direct Pay.

- Tax equity investors and syndicators evaluating or underwriting projects for 2025/26 construction.

- Architects, engineers, and EPC contractors responsible for coordinating deliverables and meeting energy thresholds.

Action Plan for Stakeholders in 2025–26

- Begin construction by July 4, 2026 via certified early expenditures or physical work;

- Include wage, apprenticeship, and bonus‑credit language in agreements immediately;

- Document all work (payments, contracts, labor logs) to support BOC and continuity safe harbor;

- Model completion timelines against market constraints—grid interconnection, equipment lead times, permitting;

- Stack bonus credit strategies (Energy Community, Domestic Content, Low-Income) where applicable.

Why You Must Act Now

Delaying past mid‑2026 will severely curtail tax credit eligibility—or eliminate it entirely—especially for solar and wind projects. Treasury’s forthcoming guidance may limit creative interpretations of “construction start,” so claim your benefits proactively rather than react retroactively.

Even a 2‑3 month delay in breaking ground could shift your project from a fully qualified 30–50% ITC to a 6% or zero-credit scenario. For high-capital projects, the difference can be in the hundreds of thousands—or millions—of dollars.

Bottom line:

Clean energy incentives under the OBBB are entering a sharp descent. To maximize credits—especially under ITC, PTC, or bonus carve-outs—you must begin construction by July 4, 2026. If you haven’t locked in contracts, financing, and project momentum now, the opportunity may already be slipping away.

Additional Planning Considerations: Timing, Stacking & Refund Opportunities for Small Businesses

The One Big Beautiful Bill Act (OBBB) not only restructured the rules around bonus depreciation, clean energy, and energy-efficient construction—but also delivered a long-overdue fix to the R&D amortization mess caused by the 2017 TCJA. For the first time, small business taxpayers who previously capitalized their domestic R&D costs under §174 may now be eligible for immediate refunds.

For businesses investing in innovation, construction, and energy-efficiency, 2025 is a year to align incentives, start early, and recover prior-year overpayments.

Small Business Refunds: Retroactive Relief from §174 Capitalization

The OBBB reinstates immediate expensing of domestic research expenditures under §174—but goes further for small taxpayers, defined as those with three-year average gross receipts ≤ $31 million under the §448(c) test.

Key opportunities:

- If you capitalized R&D expenses in 2022, 2023, or 2024, and you meet the small taxpayer definition, you may:

- Amend prior returns to fully expense those amounts, and

- Claim immediate refunds of overpaid income taxes.

- The IRS is expected to release automatic method change guidance (Form 3115) and streamlined amended return procedures before the 2025 filing season.

- If returns cannot be amended due to statute limitations, eligible taxpayers can expense capitalized costs in 2025 or ratably over 2025–2026.

Takeaway: Many small companies with legitimate R&D costs—but who deferred deductions due to §174 rules—could see tens or hundreds of thousands in refund potential by acting in early 2025.

Stacking Strategies & Interactions

Many high-impact tax incentives remain available concurrently—but require careful planning to avoid conflicts:

| Incentive | Stackable With | Notes / Conflicts |

| §174 Expensing + §41 Credit | Yes | Must coordinate §280C limitations and payroll offset interaction |

| Cost Segregation + Bonus Depreciation | Yes | Fully enhanced under OBBB for 2025+ placed-in-service assets |

| §179D + Cost Segregation | Yes, with caveats | Coordinate treatment of shared components (e.g., HVAC, lighting) |

| ITC / Energy Credits + Cost Segregation | Yes (non-overlapping) | Energy system must use MACRS 5-year schedule; cannot double-deduct solar assets |

| Direct Pay (ITC/PTC/179D) + Refund from §174 | Yes | Refunds under §174 are based on income tax, Direct Pay is refundable on its own track |

Warning: Combining R&D, cost segregation, and clean energy strategies can significantly reduce tax liability, but improper overlap or recordkeeping failures may trigger audits or recapture.

Timing Coordination: Aligning Incentives Around 2025 Deadlines

| Incentive | Critical Deadline | Action Needed |

| §174 Refund Opportunity | File amended returns in early 2025 | Confirm small taxpayer status; prepare Form 3115 or 1040X/1120X |

| §179D | Start construction by June 30, 2026 | Include labor compliance in all contracts now |

| ITC / PTC (Clean Energy) | Start construction by July 4, 2026 | Document safe harbor or physical work; confirm stacking eligibility |

| Cost Seg + Bonus | Place in service in 2025+ | Run study in coordination with ITC/179D interactions |

Strategic Compliance Checklist

- Small Business R&D:

- Confirm gross receipts test using 2022–2024 tax data.

- Flag prior returns with capitalized §174 costs.

- Prepare for amended returns and refund claims in Q1–Q2 2025.

- 179D/ITC Projects:

- Include prevailing wage & apprenticeship terms in all contractor agreements.

- Start construction planning immediately to meet mid-2026 deadlines.

- Documentation Systems:

- Establish cost centers for R&D, energy, and construction activities.

- Maintain certified payrolls, site logs, contractor agreements, and accounting memos.

Bottom line:

2025 is not just about maximizing current-year incentives—it’s also a rare opportunity to go back, fix prior compliance errors, and reclaim lost cash. Small business taxpayers who were forced to capitalize R&D may now be eligible for refunds, while large firms can stack incentives—if they align construction timing and documentation carefully.

Start now. The difference between a fully optimized incentive plan and a missed deadline could mean hundreds of thousands of dollars left with the IRS.

How Our Firm Can Help — Your Trusted Partner in 2025 Tax Incentive Planning

At Corporate Tax Advisors, we specialize in navigating the technical, engineering, and compliance hurdles that stand between you and the most valuable tax incentives in the code. With the One Big Beautiful Bill (OBBB) officially signed into law, our team is ready to help you make 2025 your most tax-efficient year yet.

We don’t just provide studies and reports — we deliver IRS-defensible documentation, strategic coordination with your CPA, and real-time support to meet critical deadlines for cost recovery and cash flow acceleration.

Our Core Services for 2025 OBBB Tax Strategy

Cost Segregation Studies

- Engineer-led site and asset-level analysis

- Compatible with 100% bonus depreciation under OBBB

- Integrated with 179D and ITC project timelines

R&D Tax Credit + §174 Compliance

- Identify qualified research activities (QRAs)

- Align payroll, contract, and prototyping costs under §41

- Prepare 2022–2024 refund-ready documentation for small businesses affected by §174 capitalization

Section 179D Energy-Efficient Deduction

- Full energy modeling (ASHRAE standards), site inspections, and allocation letters

- Contract review for prevailing wage and apprenticeship compliance

- Time-sensitive studies to meet the June 30, 2026 construction deadline

Investment Tax Credit (ITC) Planning

- Construction start documentation before July 4, 2026

- Bonus credit qualification (Domestic Content, Energy Community, Low-Income)

- Contract guidance for Direct Pay and transferability under new rules

Let’s Secure Your Incentives Before They Disappear

We are actively helping businesses across the country:

- Amend prior returns to claim §174 refunds

- Pre-certify buildings and systems for 179D and ITC before the clock runs out

- Coordinate incentive timing to avoid missed stacking opportunities

- Maximize clean energy project returns with Direct Pay + bonus credits

Don’t Wait Until Q4!

The reality is simple: If you’re not planning in Q1–Q3, you’re already behind.

Schedule your 179D or R&D eligibility review now

Request a refund estimate for prior-year §174 capitalization

Send us your contract drafts for construction projects—we’ll review them for prevailing wage & timing alignment

Contact us to set up a no-cost consultation

Let’s make 2025 the year you claim everything you’re entitled to.

Our team of CPAs, engineers, and energy modeling professionals will guide you from kickoff to compliance—and help you get paid faster by the tax code itself.

{kind=link}